Apportioned, Obligated, and Unaccounted For: Tracing ICE’s $45 Billion of Detention Funding

The White House Office of Management and Budget’s (OMB) budget records show that ICE’s detention facility expansion is already far larger and more advanced than public reporting has documented. By March 2026, OMB had apportioned more than $25 billion to expand its detention facility network, and ICE has obligated $7.9 billion of this funding.

This funding comes from a $45 billion appropriation in last year’s reconciliation law to expand DHS’s detention facility network. An internal agency planning memo said this funding will be used to buy or retrofit dozens of large detention and processing facilities, and last month budget materials released by the White House stated the funding would more than quadruple ICE’s detention capacity, from 41,500 to over 170,000 beds.

Yesterday, the Wall Street Journal reported that the DHS Inspector General has opened an audit of this spending. That article and the Journal’s earlier reporting document how DHS has paid at least $1 billion for multiple warehouses in a matter of months and that political officials pressed ICE to convert these commercial facilities into mass detention facilities by the end of this year.

But these reported purchases and contracts appear to cover only a fraction of the funding moving through OMB and ICE’s spending pipeline. OMB and Treasury Department data show ICE’s detention facility spending is far larger than what has been described in the Journal’s and other recent reporting.

The problem is that while OMB and Treasury’s data show the scale of ICE’s spending, it is incomplete. As of this writing, it appears that OMB has not released the spending plans that govern how the $25 billion of apportioned detention-facility funding will be used. Without those plans, Congress and the public cannot see which detention-facility projects OMB and ICE have approved, how much each project may receive, or whether ICE is complying with the spending plans.

What Do OMB and Treasury Department Data Show About ICE’s Detention-Facility Spending?

OMB is required by law to publish its apportionment documents. These records show when OMB makes appropriated funds available to an agency. After OMB apportions funds, the agency begins obligating the funds by entering into contracts, awarding grants, or finalizing other binding legal agreements. By law, OMB must post approved apportionments on its public website within two business days. These records are also organized and summarized on OpenOMB.org.

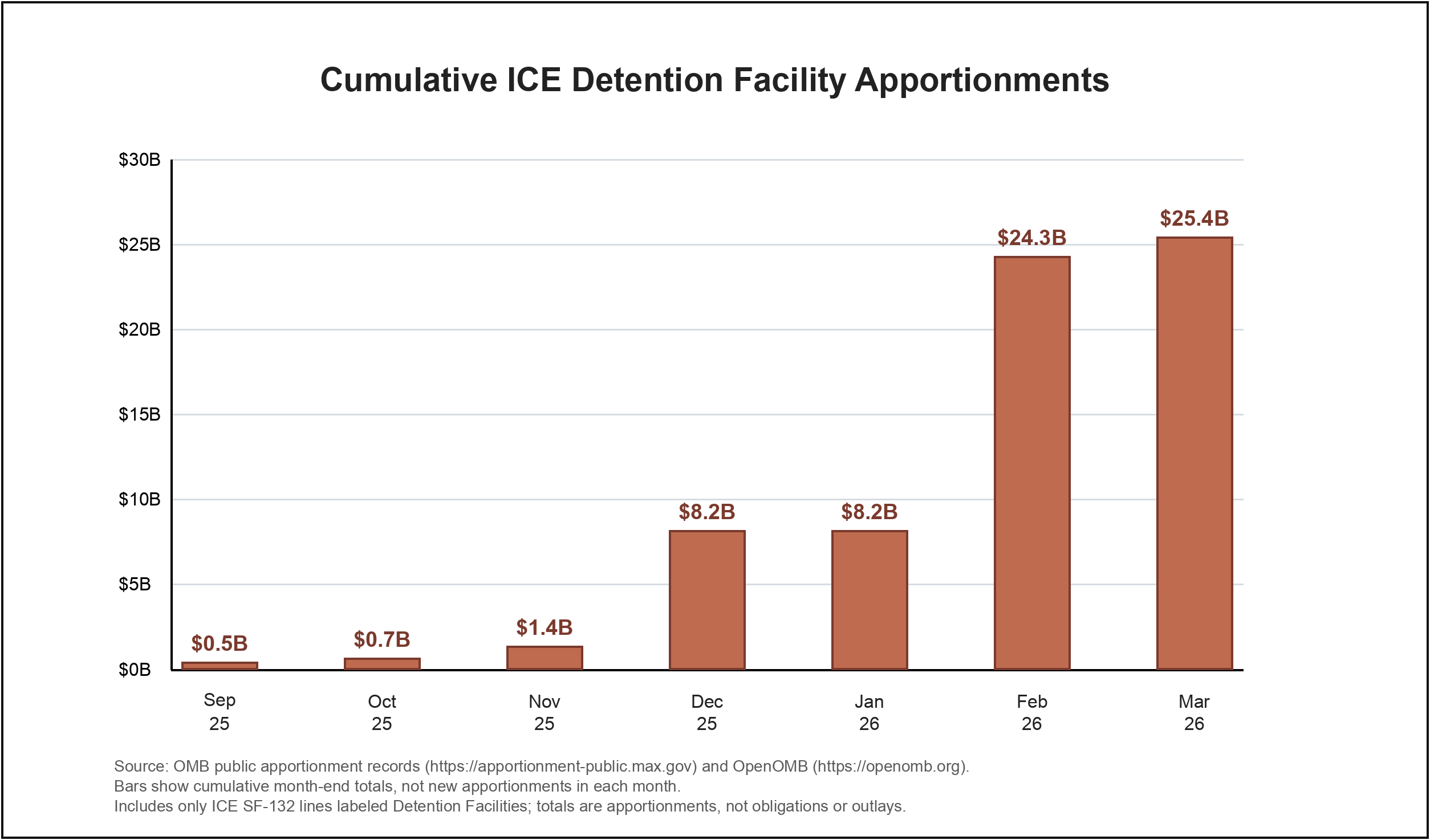

As of March, OMB’s apportionment records show that ICE’s cumulative detention facility apportionments have grown to more than $25 billion.

That amount is larger than the annual budgets of entire agencies, including NASA ($24.4 billion), the EPA ($22.3 billion), and the Department of the Interior ($17.3 billion).

Apportionment is only the first step in the federal spending process. After OMB makes funding available, an agency obligates the apportioned funding by entering into binding legal agreements. Once those agreements are executed, the Treasury Department makes cash payments, which are recorded as outlays in Treasury’s monthly and daily spending statements.

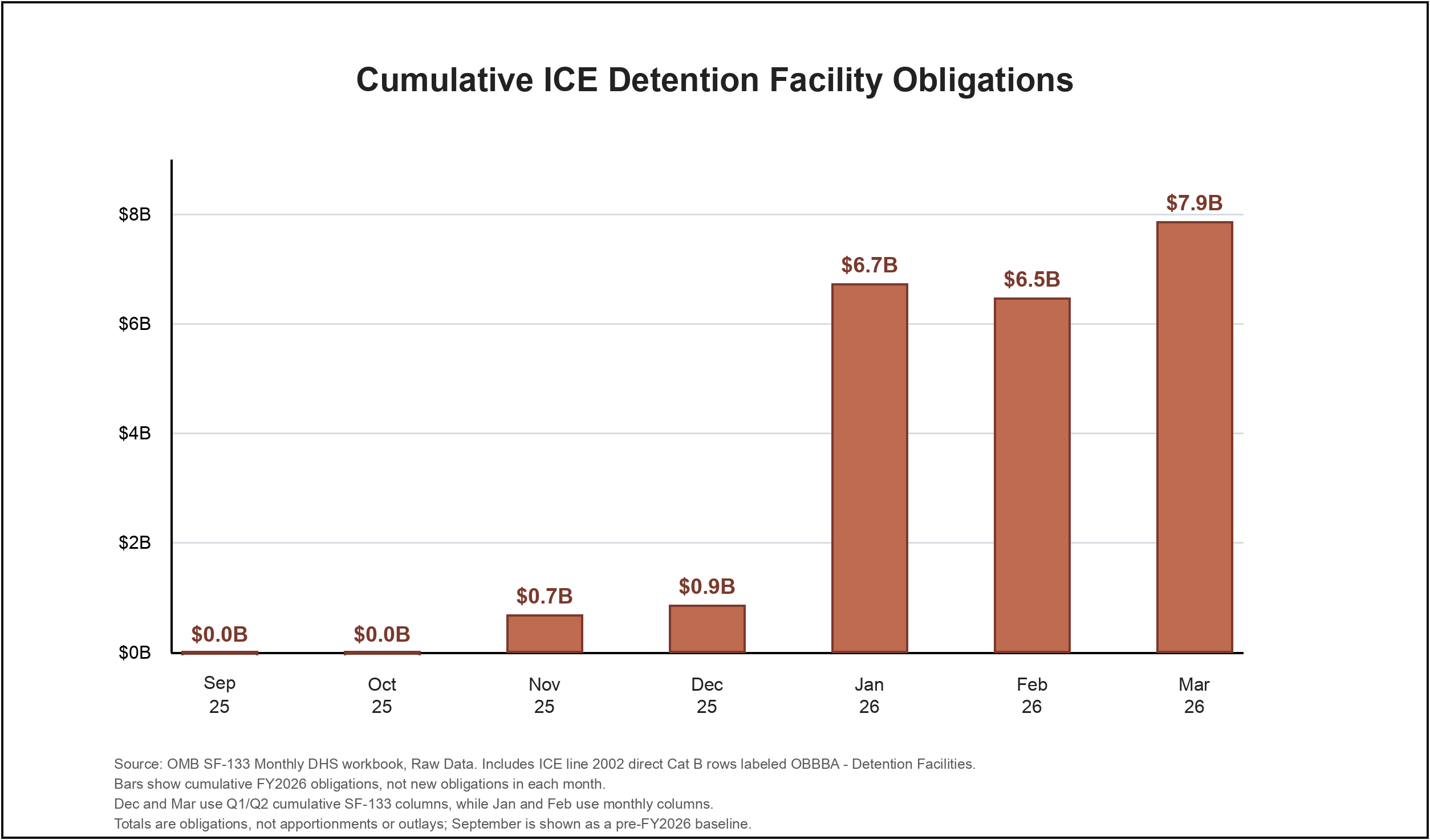

The figure below shows ICE’s cumulative detention facility obligations, reported on OMB’s SF-133 data. These obligations have also grown rapidly, reaching $7.9 billion by March - equal to roughly 80 percent of ICE’s operating budget last fiscal year.

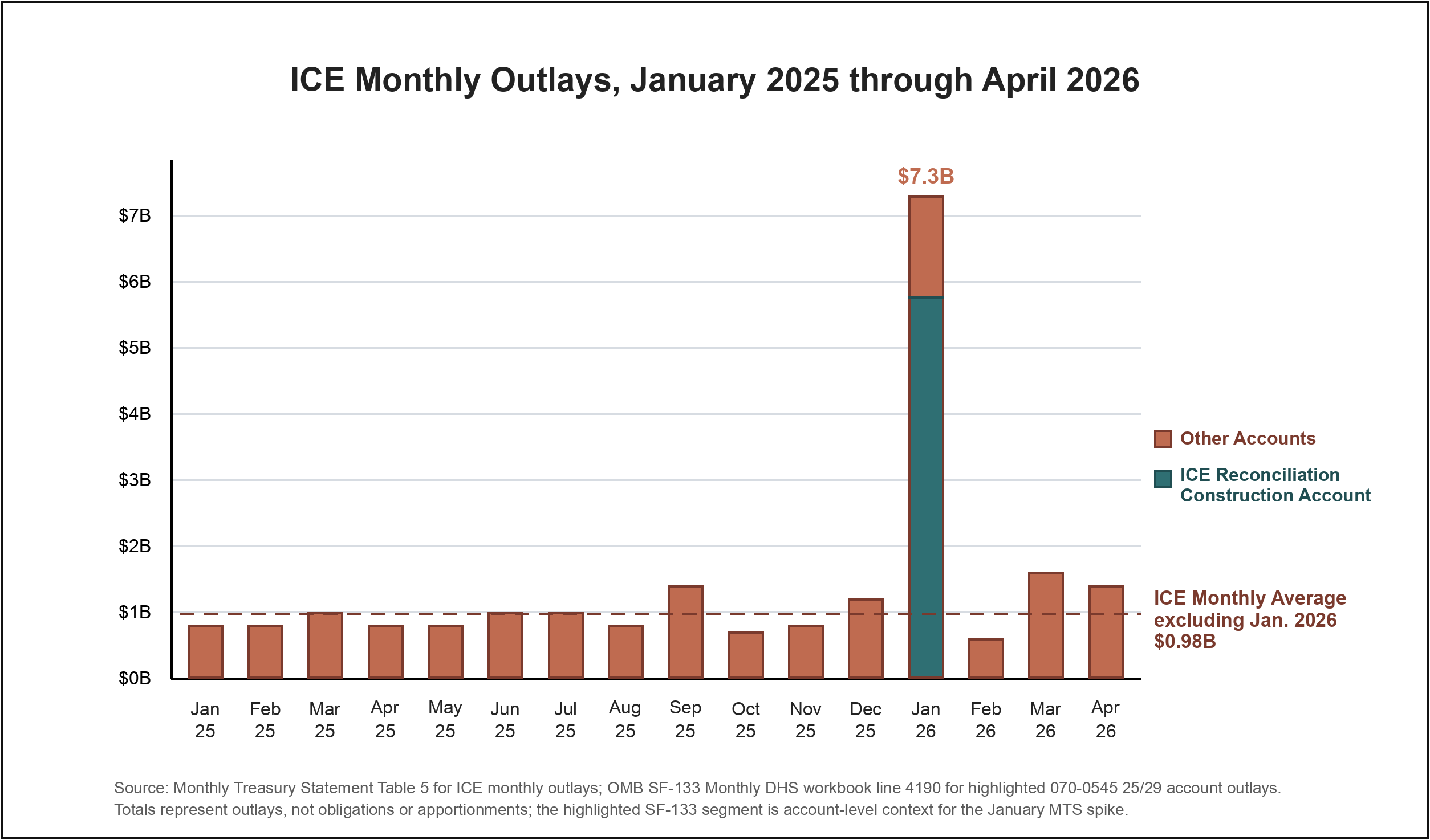

Treasury’s monthly spending data show the next stage of the spending process. In January 2026, ICE’s monthly outlays jumped to $7.3 billion, more than seven times the agency’s monthly average. Of that total, $5.8 billion came from ICE’s reconciliation construction sub-account.

Together, these records show a clear sequence. OMB apportioned $8.2 billion for detention facilities in December. In January, OMB reported $6.7 billion in cumulative ICE detention-facility obligations and that $5.8 billion was converted to outlays. OMB then apportioned another $16.1 billion for detention facilities in February. As of March, ICE had not yet obligated or spent most of that funding.

The sudden scale of these apportionments, obligations, and outlays begs the question: what, exactly, is ICE using this funding for? So far, OMB and ICE have not provided the project-level information needed to answer this question.

The Missing Link: OMB Spending Plans

When OMB apportions funding, it can use footnotes to limit how an agency uses the apportioned funding. OMB has used this authority for ICE’s detention facility apportionments. The footnotes in ICE’s Operations and Support and Procurement, Construction, and Improvements accounts state that the funds “are available for obligation solely for the projects, and at the amounts for such projects, specified in the agreed-upon spend plan between the Department of Homeland Security (DHS) and Office of Management and Budget (OMB).” In plain terms, ICE must obligate the apportioned detention-facility funding only for the projects and amounts in the agreed-upon spend plans.

In legal terms, the spend plans are “incorporated by reference” into the apportionment documents. Under a court order issued in January, OMB is required to publish these types of incorporated spending plans to its apportionment website. As of this writing, OMB appears not to have published the ICE detention-facility spend plans.

Those plans would presumably identify the facility acquisitions and renovations OMB approved and the amount ICE may obligate for each project. Without these spend plans, the public and Congress can see only the top-line apportionment amounts, not the project-level details that are controlling how ICE may use these billions of dollars.

A Larger Pattern

The apparently missing spend plans are not the only gap in the public record. They are part of a larger pattern: ICE and OMB have not provided a complete accounting of ICE’s detention-facility funding. This analysis has been able to find piecemeal information about this spending from OMB’s apportionment and SF-133 data and Treasury’s Monthly Treasury Statements. But the missing OMB spend plans, incomplete USAspending.gov data, and ICE’s most recent budget documents still leave Congress and the public without a full accounting of how ICE is using or plans to use this funding.

One example is USAspending.gov, the federal government’s spending data clearinghouse. Federal agencies are required to disclose their obligations and spending to USAspending.gov “not less frequently than monthly when practicable, and in any event not less frequently than quarterly” (31 U.S.C. 6101, note Pub. L. 109-282, sec. 3(a), as amended). It appears that DHS is using this flexibility not to report monthly obligation and spending data. While other agencies’ data are available, DHS has not posted comparable account-level spending and obligation data for the first three months of 2026. DHS has continued to report contract-related spending, but the data for ICE’s reconciliation construction account show only $25,000 of obligations in 2026 so far, a tiny fraction of the billions in 2026 outlays reported for the same account in OMB’s SF-133 data.

The same problem appears in ICE’s budget materials. Each year, agencies submit congressional budget justifications to the Appropriations Committees. These documents usually give Congress and the public a detailed account of an agency’s funding needs, planned activities, and major spending changes. ICE’s FY27 budget justification provides this detail for the agency’s annual appropriations. But it says almost nothing about how ICE is using the $45 billion of reconciliation detention-facility funding.

The Need for a Full Accounting

These discrepancies matter because the public record raises serious questions about how ICE is using this money. In March, USA Today reported that ICE purchased multiple warehouses for prices far above their assessed values, and this has been reinforced by yesterday’s Wall Street Journal reporting, as well as the Associated Press’s reporting. But, as this analysis shows, these reports still only cover a small portion of ICE’s detention-facility spending. OMB and Treasury records show billions in spending that has already occurred, plus an additional $16.1 billion in apportioned funding that ICE may be in the process of obligating.

Congress and the public need a full accounting of this funding for two reasons: to determine whether ICE is using these funds efficiently, and to determine whether the agency can safely house the people in its custody. Recent reporting has raised serious concerns about conditions inside ICE facilities, including increased violence against detainees, hunger strikes, violations of detention standards, and detainee deaths. Until OMB publishes the spend plans that were incorporated into ICE’s apportionments and DHS reports additional spending data to USAspending.gov, Congress and the public will not be able to assess how these tens of billions of dollars are being used.

Methodology

This analysis uses three public budget datasets to follow ICE detention-facility funding through the federal spending process: apportionments, obligations, and outlays. Each dataset measures a different stage of that process.

First, I used OMB apportionment records to identify when OMB made funding available to ICE for detention facilities. Apportionments are posted on OMB’s public apportionment website and are also available through OpenOMB, which makes the documents searchable. I reviewed ICE apportionments for two accounts: Operations and Support (TAFS: 070-2025/2029-0540), and Procurement, Construction, and Improvements (TAFS: 070-2025/2029-0545). Within those accounts, I counted only apportionment lines labeled for “Detention Facilities.” For each month, I used the latest approved apportionment available by the end of that month and summed the detention-facility lines across the two accounts.

To assess whether OMB had published the spend plans incorporated into these apportionment documents, I searched the “Spend Plans” folder on OMB’s apportionment website.

Second, I used OMB’s SF-133 budget-execution data for FY26 to identify detention-facility obligations. I used the FY26 Department of Homeland Security SF-133 monthly workbook and counted ICE rows for line 2002 that were labeled as direct Category B obligations for “OBBBA - Detention Facilities.” These values are cumulative fiscal-year obligations.

Third, I used the Treasury Department’s Monthly Treasury Statements to identify ICE’s agency-wide monthly outlays. Treasury’s Monthly Treasury Statement does not isolate detention-facility outlays, so I used this dataset only to show the timing and scale of ICE’s overall cash spending. For January 2026, I also used SF-133 data to show that $5.8 billion of ICE’s $7.3 billion monthly outlay spike came from ICE’s reconciliation construction account (TAFS: 070-2025/2029-0545, SF-133 line 4190).

I also analyzed DHS’s USAspending.gov data. To assess whether DHS had reported account-level obligations and outlays for calendar year 2026, I downloaded File A and File B data for calendar year 2026, which correspond to the second quarter for FY26. To assess DHS’s contract awards, I downloaded DHS’s File C data by Treasury Account and restricted the data to ICE’s reconciliation construction and procurement account (TAFS: 070-2025/2029-0545).

The analysis has important limits. Apportionments are not obligations or payments. Obligations are not cash payments. Treasury outlays show ICE-wide spending. Except for DHS’s File C data, the data used in this analysis do not identify vendors, facility addresses, contracts, or project-level details.