How Has Funding for Federal Agencies Changed Over the Last Decade?

Congress fights each year over the “topline” totals in the 12 annual appropriations acts, but these totals have become incomplete measures of federal agencies’ true budgets over the last decade. First, post-COVID inflation has eroded agencies’ purchasing power. Second, Congress has started appropriating hundreds of billions of dollars to agencies outside of the appropriations process. To address these shortcomings, I created a dataset combining agency appropriations from the annual appropriations and other laws since FY16 and adjusted the totals for inflation.

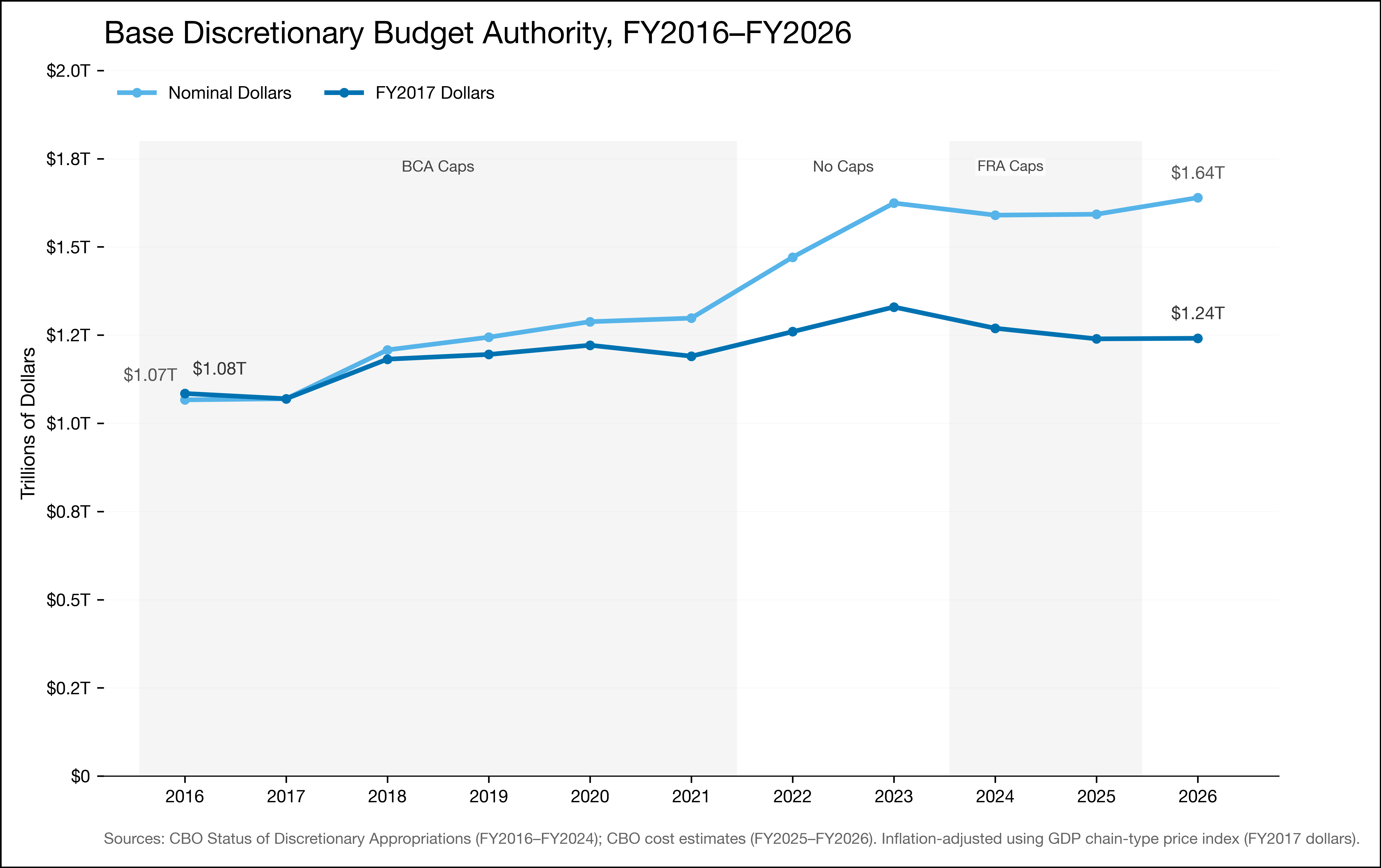

Figure 1 shows the effects of inflation on the combined top-line funding from the 12 annual appropriations acts.1 Nominally, top-line funding grew 54% over the last decade, from just over $1 trillion in FY16 to $1.6 trillion in FY26. Adjusted for inflation, however, funding increased only 14% ($156 billion) – peaking at $1.3 trillion in FY23 before declining.2 Figure 1 also shows when statutory spending caps constrained base funding during this period.3

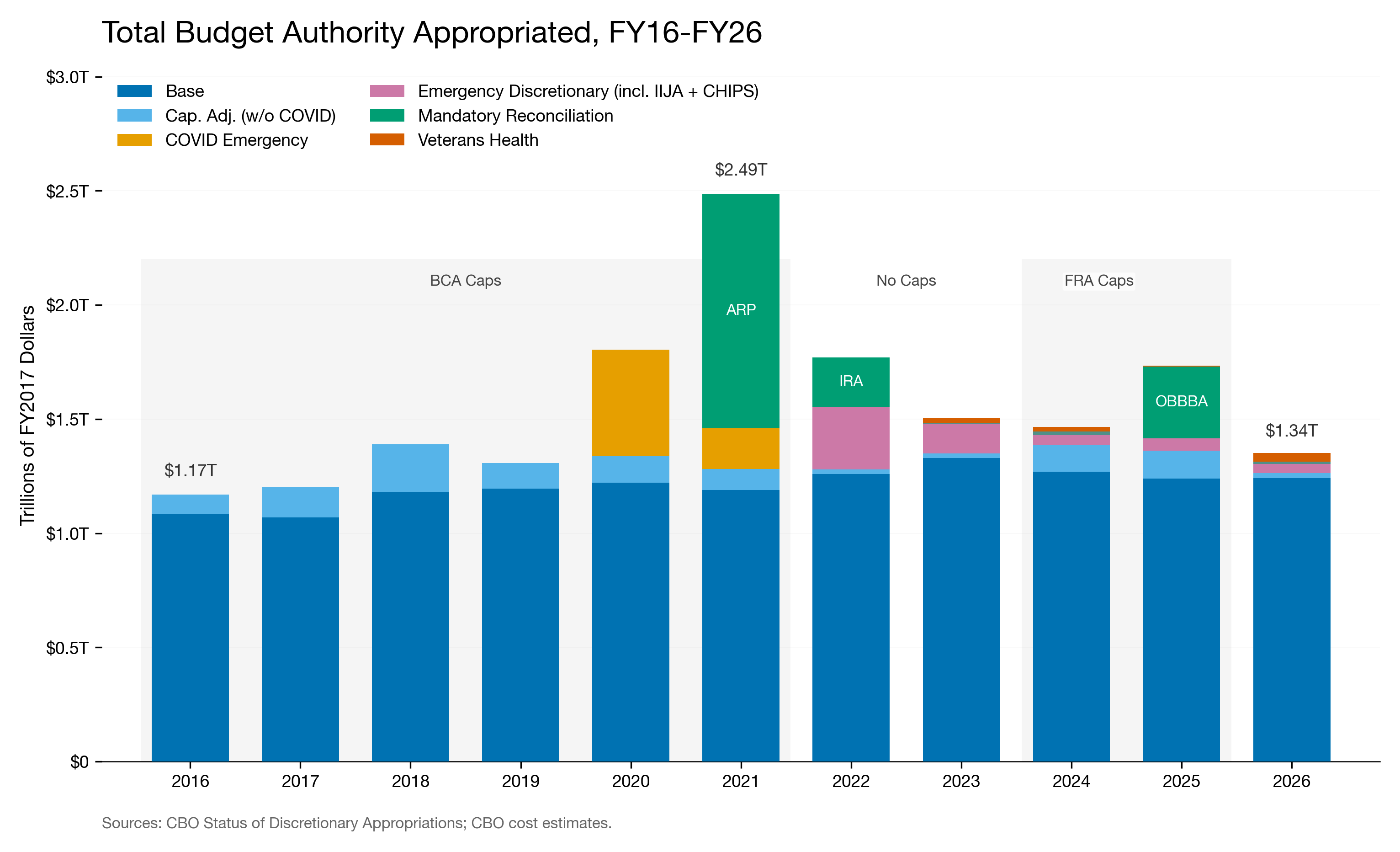

Beyond inflation, these top-line numbers exclude the hundreds of billions Congress has appropriated to agencies outside the annual process since FY20.4 In total, Congress has appropriated an additional $2.8 trillion in net real budget authority since FY20 – equal to 32% of combined top-line funding.5 Figure 2 shows these appropriations alongside the annual totals in 2017 dollars.6

Congress routed this additional funding through multiple laws, beginning with $688 billion of “emergency supplemental” appropriations in FY20 and FY21 to respond to the COVID pandemic.7 Congress regularly passes supplemental appropriations to deal with unexpected events, and they are within the jurisdiction of the Appropriations Committees. But the COVID appropriations were massive – the FY20 supplementals alone were more than twice the largest amount previously provided in a single year.8

The American Rescue Plan Act (ARPA) in 2021 signaled a more significant departure: for the first time in modern practice, Congress used a law outside the Appropriations Committees’ jurisdiction to provide long-term agency funding. Democrats set the precedent through the ARPA and the Inflation Reduction Act (IRA), which together appropriated $1.2 trillion. Both laws were enacted through “reconciliation,” part of Congress’s budget process that is protected from a Senate filibuster and routed appropriations through authorizing committees rather than the Appropriations Committees. Once Republicans gained control in 2025, they used their own reconciliation law (the so-called “One Big Beautiful Bill Act” (OBBA)) to appropriate $408 billion, primarily to the Departments of Defense and Homeland Security. Because these laws were not within the jurisdiction of the Appropriations Committees, their appropriations were scored as “mandatory spending.”

Congress also passed bipartisan laws with long-term appropriations outside of the annual process. The two largest – the Infrastructure Investment and Jobs Act (IIJA) and the CHIPS and Science Act – together appropriated $471 billion.9 Under the jurisdictional logic that classified reconciliation funding as mandatory, these appropriations would have been scored the same way. But Congress instead designated the funds as “emergency discretionary” spending. On paper, though, the mandatory reconciliation and emergency discretionary appropriations look the same: each appropriated specific dollar amounts to agencies for multi-year use. Whether the spending was labeled as mandatory or discretionary depended on the procedural and political obstacles facing each law, not the nature of the spending itself.

The labels — mandatory and discretionary — originally reflected Congress’s traditional internal division of spending labor. Congress delegated control of discretionary spending to the Appropriations Committees’ annual appropriations, and control of mandatory spending to other committees, primarily the House Ways & Means Committee and Senate Finance Committee. For decades, the jurisdictional line corresponded to a substantive one: discretionary spending funded agency operations through annual and supplemental appropriations, and mandatory spending funded entitlement programs like Social Security and Medicare.

The COVID supplementals, even at their massive scale, stayed within this framework. Since 2021, Congress has broken it. Reconciliation funding is formally mandatory because authorizing committees, not the Appropriations Committees, control the bills — but OBBA’s $332 billion to Defense and Homeland Security funds agency operations, not entitlements.10 The emergency discretionary label tells the opposite story: Congress classified IIJA and CHIPS Act funding as discretionary not because the Appropriations Committees controlled it, but to avoid PAYGO rules that apply to mandatory spending and require dollar-for-dollar budgetary offsets.

The PACT Act created a third funding mechanism that further underscores how the discretionary topline fails to capture the full cost of agency operations. When Congress expanded healthcare for veterans with toxic exposures in 2022, it froze the Veterans Affairs’ (VA) discretionary funding of these services at FY21 levels and created the Cost of War Toxic Exposures Fund (TEF) to cover all costs above that baseline. Unlike the reconciliation and emergency appropriations, which were for specified amounts, appropriations to the TEF are open-ended — the statute authorizes “such sums as are necessary” above FY2021 levels.11 Because the baseline was not adjusted for inflation, an increasing share of what would otherwise be discretionary VA spending flows through the TEF instead.

The appropriations to the TEF are, for budget scorekeeping purposes, invisible. The statute gave them a unique scoring treatment: they are classified as direct spending in CBO’s baseline projections but counted as neither discretionary budget authority nor direct spending when CBO scores the appropriation acts that actually fund them. TEF dollars therefore do not appear in the cost estimates that drive the annual appropriations debates.12 The Fund’s appropriations have grown rapidly — from $5 billion in FY2023, to $52.7 billion in FY2026, with projections exceeding $400 billion through 2035.13 Since 2022, over $110 billion in agency funding that would have appeared in the VA’s discretionary topline has instead been provided through a fund that is invisible in the cost estimates Congress uses to debate annual spending levels.

Taken together, inflation and these new funding mechanisms have made the topline amounts at the center of the annual appropriations debate an increasingly unreliable guide to agency funding. Congress is now appropriating trillions of dollars through legislation that carries less oversight, less annual review, and less public scrutiny than traditional discretionary spending — and its budget procedures have not adapted. This is the first in a series of posts that will use original data and empirical analysis to examine underappreciated aspects of how Congress budgets and spends.

Correction: The second graphic was updated on May 18, 2026 to correct an error. In the original version of the graphic, the outlays of the CHIPS and Science Act were erroneously classified as mandatory reconciliation outlays. The current graphic correctly labels these outlays as emergency discretionary outlays.

Methodology

This analysis uses a unified FY2016–FY2026 budget authority dataset that combines annual discretionary appropriations with funding Congress appropriated through other legislative vehicles. Figure 1 draws on the Congressional Budget Office’s (CBO) Status of Appropriations data for FY16–FY25; FY26 amounts were compiled from the enacted appropriations acts and CBO’s most recent score of a continuing resolution for the Department of Homeland Security (P.L. 119-37) (see supra footnote 1).

Figure 2 adds appropriations from ten additional public laws, including reconciliation laws (the American Rescue Plan Act, Inflation Reduction Act, and One Big Beautiful Bill Act), emergency supplementals and other discretionary vehicles (the IIJA, CHIPS and Science Act, and annual appropriations acts containing emergency-designated funding), and the PACT Act’s Toxic Exposures Fund.14

These amounts were drawn from CBO cost estimates and include only new appropriations of budget authority to federal agencies. The dataset excludes changes to mandatory spending that resulted from statutory modifications to entitlement programs, tax provisions, or other non-appropriations budgetary effects except for appropriations connected to the PACT Act’s Toxic Exposures Fund.

All amounts are reported in fiscal years and adjusted for subsequent rescissions. Nominal dollars are converted to real FY2017 dollars using the GDP chain-type price index from the Congressional Budget Office.15

Footnotes

FY16-FY25 budget authority was taken from annual files available at Congressional Budget Office, Status of Appropriations. As of this writing, 11 of the 12 annual FY26 appropriations have been enacted and the Department of Homeland Security’s annual appropriation has not been approved. FY26 budget authority is the sum of the enacted budget authority and DHS’s annualized spending under the most recent continuing resolution. See, Congressional Budget Office, Senate Amendment 3937 to H.R. 5371, the Continuing Appropriations, Agriculture, Legislative Branch, Military Construction and Veterans Affairs, and Extensions Act, 2026 (November 10, 2025); H.R. 6938, Commerce, Justice, Science; Energy and Water Development; and Interior and Environment Appropriations Act, 2026 (January 6, 2026); H.R.7006 - Financial Services and General Government and National Security, Department of State, and Related Programs Appropriations Act, 2026 (January 14, 2026); H.R. 7148, Consolidated Appropriations Act, 2026 (January 21, 2026).↩︎

Figure 1 only shows the “base” budget authority appropriated by the annual appropriations acts, excluding additional supplemental and emergency appropriations funding commonly known as “cap adjustments” — additional appropriations Congress exempts from statutory spending caps for specific programs like disaster relief and veterans’ healthcare. From FY16-FY26, these adjustments added $2.2 trillion in real budget authority, equal to 17% of base funding over the same period. See, Budget Counsel, Cyclopedia of Congressional Budget Law: Cap Adjustment.↩︎

The Budget Control Act of 2011 (P.L. 112-25) established annual limits on base discretionary budget authority for FY12-21. These limits were modified by P.L. 112-240, P.L. 113-67, P.L. 114-74, P.L. 115-123, P.L. 116-37. No caps were in place for FY22 and FY23. The Fiscal Responsibility Act (P.L. 118-5) established caps for FY24 and FY25.↩︎

The laws that provided mandatory funding are: P.L. 117-2, P.L. 117-169, P.L. 117-167, P.L. 118-5, P.L. 119-21. The discretionary emergency spending were provided by: P.L. 116-20, P.L. 116-26, P.L. 116-113, P.L. 116-123, P.L. 116-127, P.L. 116-13, P.L. 116-139, P.L. 117-43, P.L. 117-58, P.L. 117-70, P.L. 117-103, P.L. 117-128, P.L. 117-128, P.L. 117-159, P.L. 117-167, P.L. 117-180, and P.L. 117-328.↩︎

This excludes an additional $558 billion of non-COVID “cap-adjustment” appropriations since FY20, which were appropriated in addition to the base amounts. These include Overseas Contingency Operations/Global War on Terror funding, disaster relief, program integrity, wildfire suppression, and non-COVID emergency-designated funding that adjusted the statutory caps. These amounts are shown in light blue in Figure 2.↩︎

Figure 2 excludes the mandatory spending effects of statutory changes to entitlement programs, except for the Honoring our PACT Act expansion of veterans’ health care for toxic exposures.↩︎

Amount in nominal dollars, as are all subsequent amounts.↩︎

Congressional Budget Office, Supplemental Appropriations Enacted Since Fiscal Year 2000 (as of December 21, 2024).↩︎

The Bipartisan Safer Communities Act (P.L. 117-159) included $4.6 billion of similar multi-year discretionary appropriations.↩︎

The law contains $77 billion of additional appropriations to other agencies.↩︎

Honoring Our PACT Act (P.L. 117-168), section 805(c).↩︎

Id.↩︎

See, Department of Veterans Affairs, FY2026 Budget Submission. The FY26 Military Construction, Veterans Affairs and Related Agencies Appropriations Act appropriated $52.7 billion to the fund, see 139 Stat. 608.↩︎

They are: the American Rescue Plan Act (P.L. 117-2), CHIPS and Science Act (P.L. 117-167), Sergeant First Class (SFC) Heath Robinson Honoring our Promise to Address Comprehensive Toxics (PACT) Act (P.L. 117-168), Inflation Reduction Act (P.L. 117-169), the Consolidated Appropriations Act, 2023 (P.L. 117-328), Fiscal Responsibility Act (P.L. 118-5), Veterans Benefits Continuity and Accountability Supplemental Appropriations Act, 2024 (P.L. 118-82), Full-Year Continuing Appropriations and Extensions Act, 2025 (P.L. 119-4), One Big Beautiful Bill Act (Public Law 119-21), and Continuing Appropriations, Agriculture, Legislative Branch, Military Construction and Veterans Affairs, and Extensions Act, 2026 (P.L. 119-37).↩︎

Congressional Budget Office, Historical Data and Economic Projections, Feb 2026, Annual_FY_February2026.csv.↩︎