How Have ICE and CBP Used Their $140 Billion from the One Big Beautiful Bill?

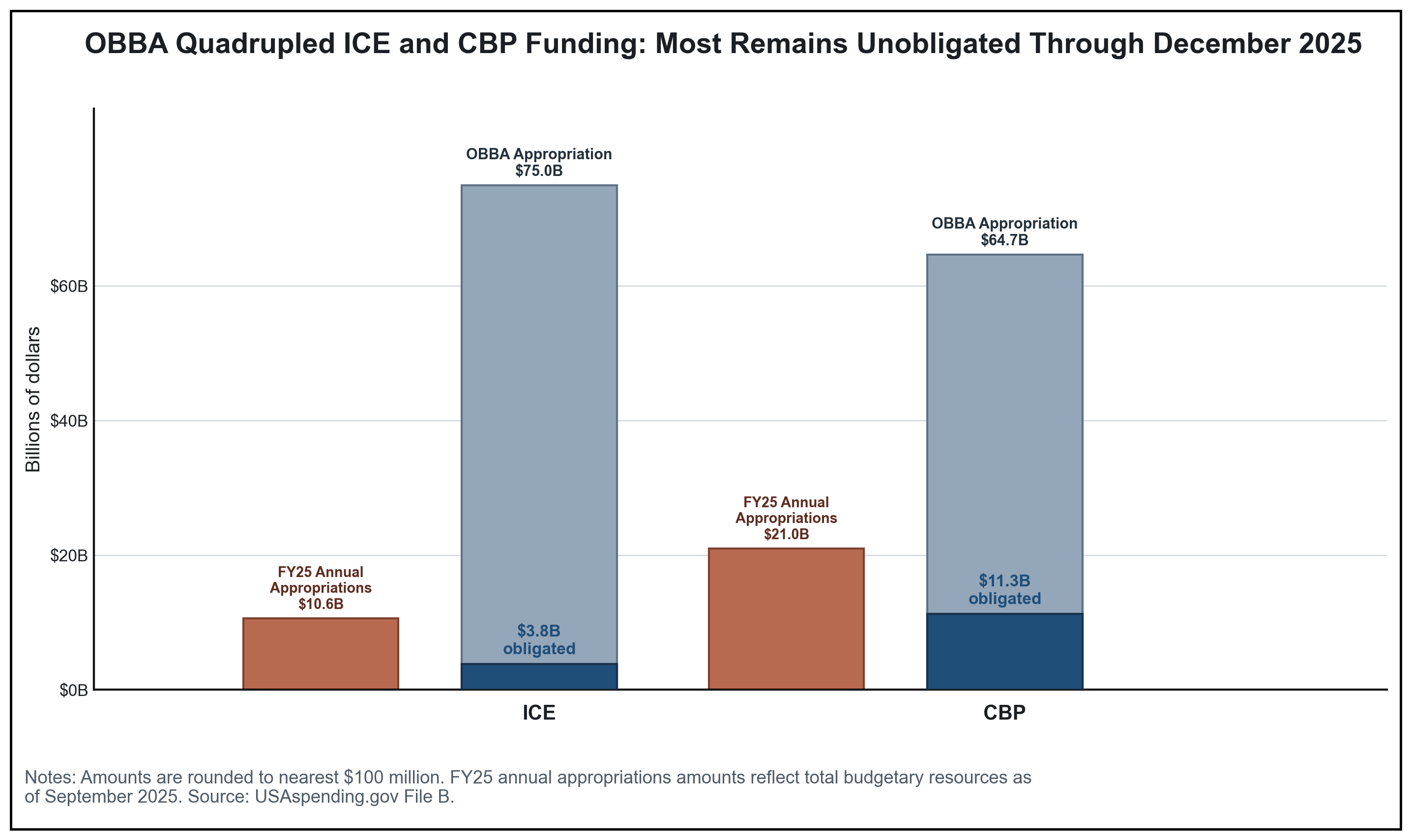

The Department of Homeland Security (DHS) has been shut down since February 14, 2026, and the public debate is now focused on how much additional funding Immigration and Customs Enforcement (ICE) and Customs and Border Protection (CBP) should receive in a new reconciliation bill. But the Trump Administration has not fully disclosed how it has used the $139.6 billion of multiyear funding that Congress appropriated to the two agencies in last year’s reconciliation bill, the One Big Beautiful Bill Act (OBBA). OBBA, enacted last July, gave ICE and CBP more than four times their combined prior-year budgets. The best available data shows that, as of December 2025, ICE had obligated $3.8 billion (5%) of its $74.9 billion. CBP had obligated $11.3 billion (17%) of its $64.7 billion. Together, the two agencies had obligated just $15.1 billion (11%) of the $139.6 billion OBBA appropriated to them. My analysis below shows that the administration used OBBA’s funding in 2025 to supplement, not replace, ICE and CBP’s annual appropriations.

Whether that pattern still holds during the current shutdown is unclear. USAspending.gov, the primary source for this analysis, includes DHS spending data through December 2025 but no DHS data for 2026, even though other agencies have reported 2026 data. Without this information, the public cannot track how the administration is spending OBBA’s remaining $124.5 billion balance for ICE and CBP.

Tracing How CBP and ICE Used OBBA Funding in 2025

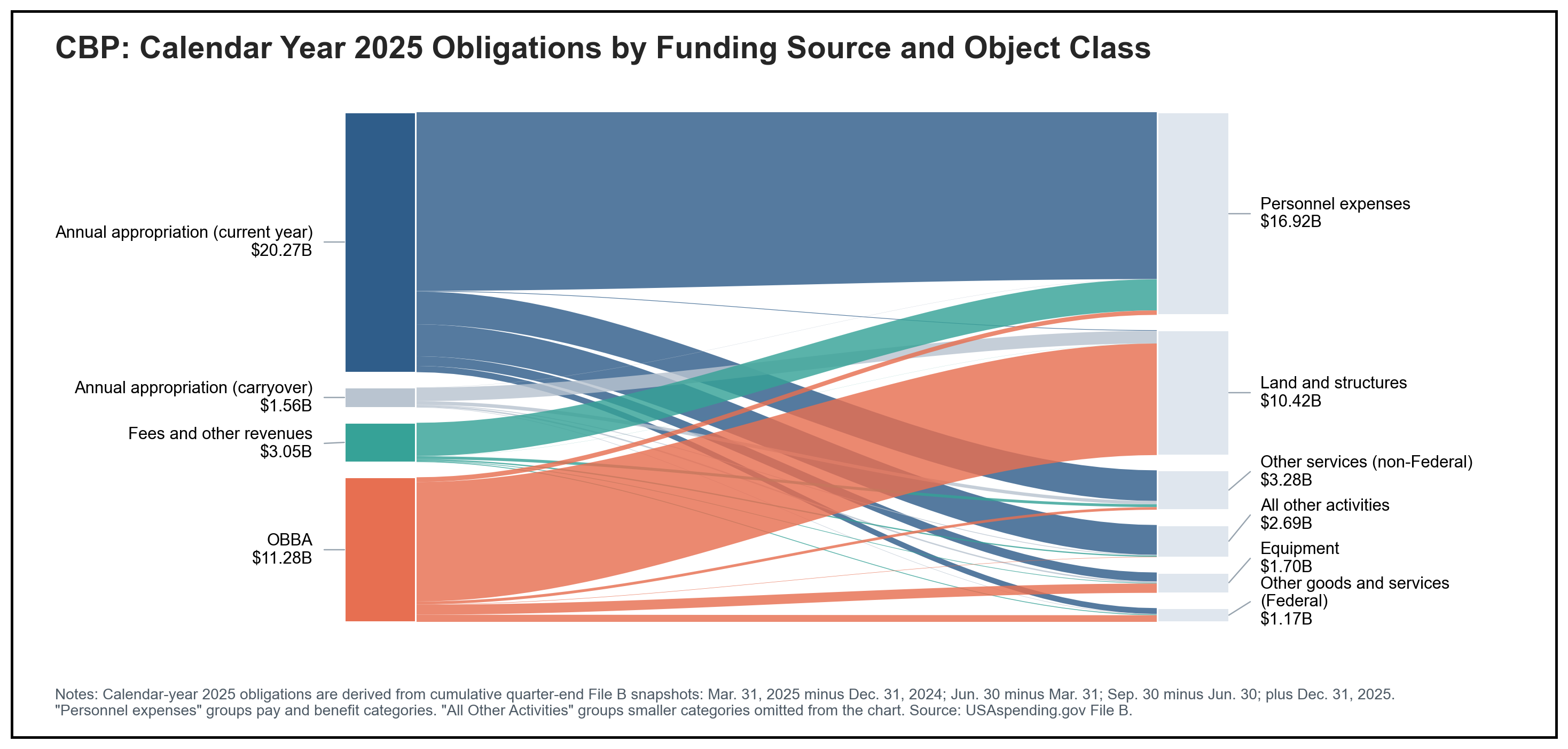

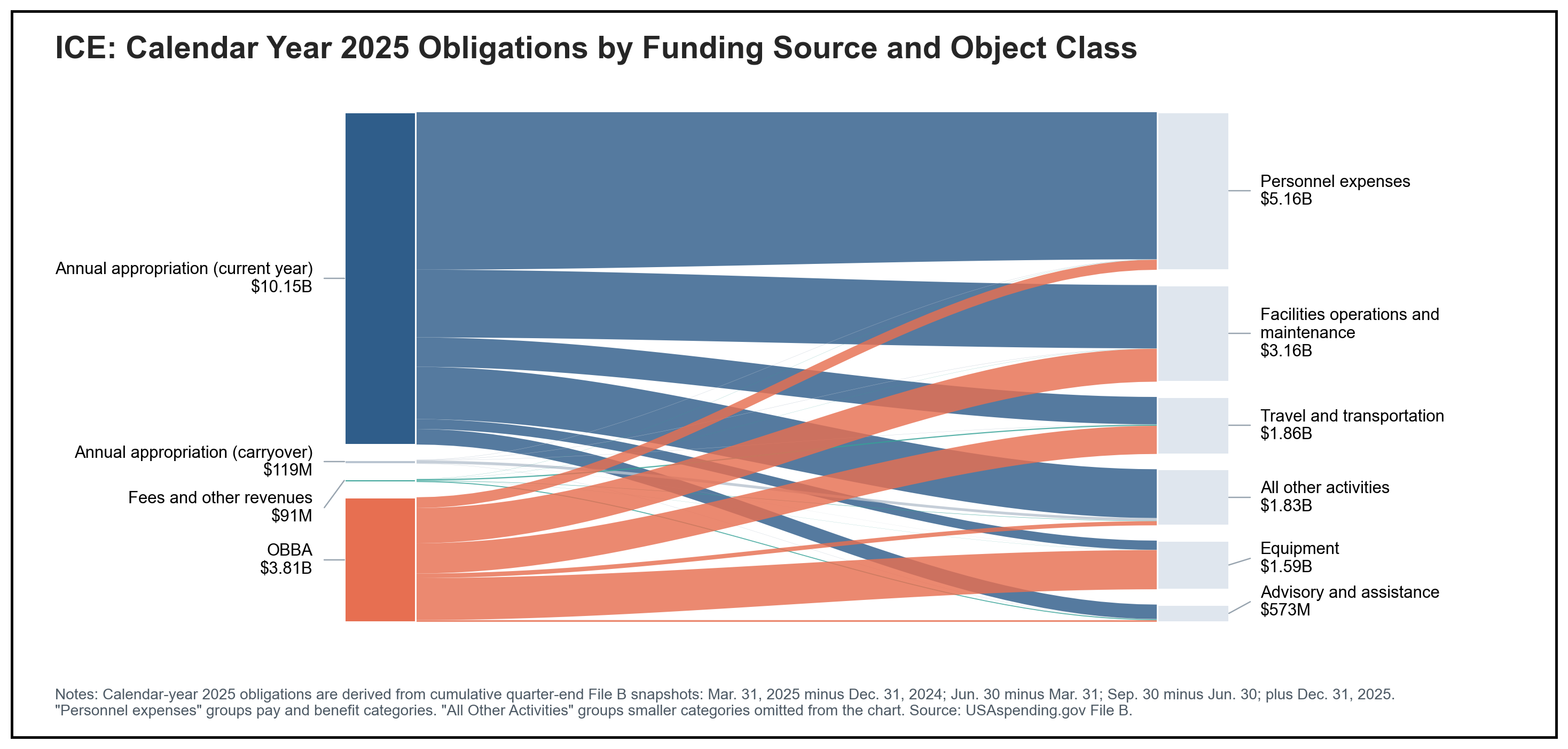

I structured my analysis around two questions. First, how much of ICE and CBP’s spending in 2025 came from their annual appropriations versus OBBA? Second, what did each funding source pay for? The Sankey diagrams below answer both questions by tracing each agency’s 2025 obligations from their funding source on the left to their spending category on the right.

Two patterns are immediately visible. First, the agencies used OBBA for different purposes. CBP obligated $9.2 billion – 82% of its OBBA obligations – to land and structures, consistent with the administration’s expansion of border wall construction projects. ICE obligated 86% of its OBBA obligations to equipment ($1.3 billion), facilities operations and maintenance ($1.1 billion), and travel and transportation ($922 million), likely using these funds to expand detention and removal operations. Second, neither agency used OBBA to substitute for the personnel costs funded by their annual appropriations. OBBA covered just 2% of CBP’s $16.9 billion in personnel obligations and 6% of ICE’s $5.2 billion total personnel costs.

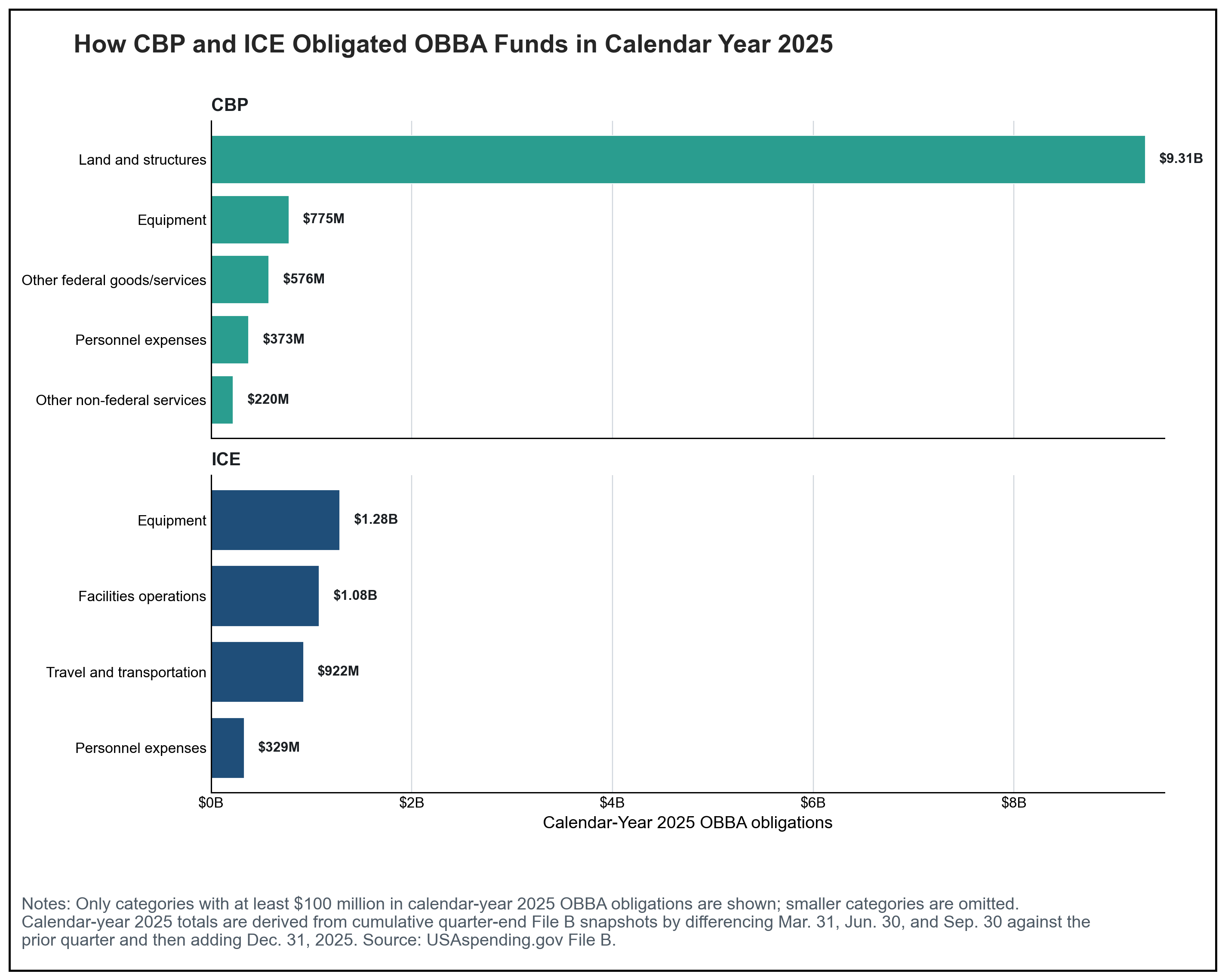

The third figure below breaks down what each agency’s OBBA obligations paid for in more detail, showing how the funds were primarily used for facilities, land, and equipment, rather than personnel costs.

OBBA’s statutory text and DHS’s administrative actions during last year’s government shutdown (October 1-November 12) help explain these patterns. Both agencies’ OBBA personnel funds were appropriated for “hiring and training additional” staff, not for paying the existing workforce funded through annual appropriations. DHS’s shutdown plan reflected this distinction: it classified “personnel required to provide direct staff support to execution of Public Law 119-21 [OBBA]” as “excepted,” meaning they had to work without pay.

DHS appears to have followed this guidance for three weeks, until DHS Secretary Kristi Noem announced that 70,000 DHS law enforcement officers, including those at CBP and ICE, would receive a “super check” covering all hours worked during the shutdown plus their next pay period. CBP told employee union representatives that a “reclassification of the funding source” made the payments possible, though neither CBP nor DHS disclosed which accounts were used. The full-year spending data bears this out: OBBA covered a small fraction of each agency’s personnel costs.

Current Policy Uncertainty

The 2025 analysis cannot be directly extended to the current shutdown because it appears that DHS has stopped reporting spending data to USAspending.gov. The lack of spending information means that neither the public nor Congress can track how the administration is drawing down OBBA’s remaining $124.5 billion balance for ICE and CBP.

News reporting throughout the shutdown suggests the administration has used OBBA funds more aggressively this time. In February, CBP exempted as many as 57,600 employees using OBBA funding – roughly 30% more than the total number of exempt employees in DHS’s 2025 shutdown plan for the entire department. In late March and early April, President Trump directed DHS to use funds with “a reasonable and logical nexus” to pay TSA employees and then all remaining DHS employees. The New York Times reported that these payments were funded by OBBA and structured as a temporary bridge. Employees received a paycheck on April 10, but DHS told them they would not be paid again until Congress restored annual funding. But without up-to-date spending data, it is not possible to know.

The Upcoming Debate

President Trump, Speaker Johnson, and Majority Leader Thune have announced a plan to fund ICE and CBP for the rest of the Trump Administration through budget reconciliation – the same process Congress used for OBBA – by June 1. Congress and the public are now debating how much additional funding the agencies should receive without a proper accounting of what funding the agencies have. This analysis shows that the agencies had approximately $124.5 billion in unobligated OBBA funding at the end of 2025 – equal to more than four years of their combined annual budgets before OBBA. Even with this much funding available, ICE and CBP funded last year’s enforcement operations – including in the Twin Cities, Chicago, Los Angeles, and communities across the country – primarily through their annual appropriations, not OBBA.

Before debating how much more funding ICE and CBP need, Congress and the public need to know how much of the remaining $124.5 billion the administration has already spent this year and what it plans to do with the rest. Until these questions are answered, Congress will be legislating blindly.

Correction (April 17): An earlier version of this analysis rounded ICE’s total OBBA appropriation to $75 billion. The correct figure is $74.9 billion. Affected amounts in the first figure and the text have been updated. (April 19): Figure 1 was updated to more accurately describe the source data used to generate the figure.

Methodology

This analysis is based on File A and File B data downloaded from USAspending.gov during the weeks of April 6 and April 12, 2026.

Because USAspending.gov’s quarterly File B data record cumulative obligations and outlays within each fiscal year, the calendar-year 2025 analysis converted quarter-end cumulative obligations into quarter-over-quarter differences and then recombined those differences into calendar-year totals. The resulting calendar-year series covers four intervals: December 31, 2024 to March 31, 2025; March 31 to June 30, 2025; June 30 to September 30, 2025; and October 1 to December 31, 2025.

To identify the Treasury accounts associated with the Department of Homeland Security (DHS), U.S. Immigration and Customs Enforcement (ICE), and U.S. Customs and Border Protection (CBP), the analysis relied on the Department of the Treasury’s Federal Account Symbols and Titles (FAST) Book, Parts II and III.

Funding was classified into four categories using each Treasury Appropriation Fund Symbol (TAFS): current-year annual appropriations, carryover balances from prior annual appropriations, fee and other revenues, and appropriations provided by the One Big Beautiful Bill Act (OBBA; P.L. 119-21). The classifications were principally based on each TAFS’s period of availability. TAFS were classified as current-year annual appropriations if their availability began and ended in fiscal year 2025 or fiscal year 2026. They were classified as carryover balances if they became available before fiscal year 2025 but remained available in fiscal years 2025 or 2026. TAFS with a period of availability of “-X-” were classified as “fee and other revenues” accounts because most of the budgetary resources in these accounts were tied to fee collections, with one exception explained below. TAFS were classified as OBBA appropriations if they began in fiscal year 2025 and remained available through fiscal year 2029 or fiscal year 2034, which are consistent with the statutory text of the law’s appropriations to DHS. The main exception to these classifications was CBP’s TAFS 070-X-0532-000. This TAFS was classified as an OBBA appropriation because the program activity name in the USAspending.gov File B data identified it as being connected to OBBA section 90002.

The table below maps the principal OBBA appropriations to components of DHS related to immigration enforcement and border security. Because there is no authoritative statutory-to-TAFS crosswalk, the table identifies the primary or candidate TAFS associated with each OBBA appropriation based on Treasury account titles, periods of availability, and OBBA’s statutory text.

| OBBA Provision | Statutory Amount ($, Billions) | Statutory recipient / purpose | TAFS Mapped to Provision | Included in ICE/CBP analysis? | Notes |

|---|---|---|---|---|---|

| Sec. 90001 | $46.55 | CBP border infrastructure and wall system | 070-2025/2029-0532-000 | Yes, CBP | TAFS’s availability matches OBBA, File B mentions OBBA |

| Sec. 90002 | $12.01 | CBP personnel, bonuses, vehicles, and facilities | 070-2025/2029-0530-000; 070-X-0532-000 | Yes, CBP | TAFSs’ availability matches OBBA, File B mentions OBBA |

| Sec. 90003 | $45.00 | ICE detention capacity | 070-2025/2029-0540-000 | Yes, ICE | TAFS’s availability matches OBBA |

| Sec. 90004 | $6.17 | CBP border security, technology, and screening | 070-2025/2029-0530-000; 070-2025/2029-0532-000 | Yes, CBP | File B mentions OBBA |

| Sec. 90005(a) | $2.58 | FEMA-administered state and local assistance | FEMA grant accounts | No | Outside the ICE/CBP analysis |

| Sec. 90005(b)(3) | $10.00 | DHS State Border Security Reinforcement Fund | 070-2025/2034-0722-000 | No | DHS-wide support account; outside the ICE/CBP analysis |

| Sec. 90007 | $10.00 | DHS border support reimbursement | 070-2025/2029-1917-000 | No | DHS-wide support account; outside the ICE/CBP analysis |

| Sec. 100051 | $2.06 | Secretary of Homeland Security appropriation | 070-2025/2029-0100-000; 070-2025/2029-0406-000 | No | Appropriated to DHS Secretary; outside the ICE/CBP analysis |

| Sec. 100052 | $29.85 | ICE enforcement appropriation | 070-2025/2029-0540-000; 070-2025/2029-0545-000 | Yes, ICE | TAFS’s availability matches OBBA |

| Sec. 100053 | $0.75 | Federal Law Enforcement Training Centers | 070-2025/2029-0509-000; 070-2025/2029-0510-000 | No | Appropriated to DHS Secretary; outside the ICE/CBP analysis |

This analysis classified the following TAFS as ICE and CBP’s primary OBBA accounts: 070-2025/2029-0540 (Operations and Support) and 070-2025/2029-0545 (Procurement, Construction, and Improvements) for ICE, and 070-2025/2029-0530 (Operations and Support), 070-2025/2029-0532 (Procurement, Construction, and Improvements), and 070-X-0532 (Procurement, Construction, and Improvements) for CBP. The combined budget authority in these accounts closely matches OBBA’s statutory appropriations to each agency. As of September 2025, CBP’s TAFS contained $64.8 billion, compared to $64.7 billion appropriated by OBBA sections 90001, 90002, and 90004. ICE’s two TAFS held $74.87 billion in budget authority, compared to the $74.9 billion appropriated to ICE under OBBA sections 90003 and 100052.

In December 2025, an additional $15.8 billion in budgetary resources was reported in ICE’s 070-2025/2029-0545 TAFS. This analysis excludes the $15.8 billion from all calculations because the information in the USAspending.gov data does not link this funding conclusively to OBBA. Additionally, this analysis excludes other DHS TAFS not listed in the table above that received OBBA appropriations because those funds were appropriated to DHS components other than ICE and CBP.

The headline comparison between ICE and CBP’s OBBA obligations and the total budget authority appropriated by OBBA uses calendar-year 2025 obligations from the core TAFS identified above as the numerator and enacted OBBA appropriations as the denominator.

The classification of obligations by object class in the subsequent diagrams relied on the Office of Management and Budget’s definition of object classes from Circular A-11, which categorizes federal obligations by the type of good or service acquired, including personnel compensation, travel and transportation, equipment, and numerous additional categories.

Dollar amounts above $1 billion were rounded to the nearest $100 million. Percentages were calculated on unrounded amounts.